Interest rates and high purchase prices are pushing a lot of people away from buying. Most are turning to renting, but is that the best move right now? Will House Hacking prove to be better than Renting over the span of the next 5 years? That’s what this blog is all about. To effectively evaluate the financial implications of renting versus house hacking, we’ll dive deep into the numbers and walk you through how we calculated them. We’ll also make sure to address the opportunity costs associated with Renting and House Hacking.

Here are the numbers we are going to use in this blog. They are very realistic numbers for what you would experience as a house hack buyer or renter in Colorado Springs.

Buyer – Buying a 450k home at a 6.625% interest rate with a 5% downpayment ($22,500). The home has 5 bedrooms and you are renting out four of them for $600 each ($2,400).

Renter – You are paying $1,200 in rent for a decent 1 bedroom apartment in Colorado Springs. You just signed a year lease. According to Apartments.com the average rent of a 1 bedroom apartment in Colorado Springs is $1,308/month and only 662sqft.

When you rent you are giving up a lot of the benefits of owning. We will start with those. Then we will talk about what you give up when you House Hack. Focusing purely on the numbers.

Opportunity Cost of Renting: No Appreciation

Let’s start by understanding the concept of appreciation in the context of real estate. Appreciation refers to the increase in a property’s value over time. Since 1993 (the oldest median sales price data from Pikes Peak Association of Realtors) homes have appreciated at a rate of 5.38% per year. (Median price in Jan. 1993 $88,775. Median Price in Jan. 2023 $450,000). For that reason, we will assume a smaller 4.5% for the annual appreciation of real estate in Colorado Springs.

To calculate the total appreciation value at the end of five years, we use the formula:

Future Value = Present Value × (1+Appreciation Rate)^n

For a property with a purchase price of $450,000 and an annual appreciation rate of 4.5%, the value after 5 years can be calculated as follows:

Future Value = 450,000 × (1+0.045)^5 = 560,781.8719

560,781.87 – 450,000 = 110,781.87. This is the amount of value you are expected to gain in the next 5 years. This is a very real value that you can cash in on by selling the property or pulling a HELOC and reinvesting.

Appreciation details and assumptions:

While real estate appreciation is not guaranteed, historical trends can offer some predictive insight. It’s essential to recognize that all investments carry assumptions and risks, but informed decisions are based on historical data and trends. We showed above how we got the 5.38% annual appreciation and we chose a more conservative number of 4.5% annual appreciation.

One of the unique advantages of real estate investment is leveraged appreciation. By putting down a small percentage of the property’s value (e.g., 5%), you control 100% of the property and benefit from 100% of the appreciation, despite the bank financing the majority of the purchase.

What do I mean by that? Let me set up an example here. Let’s say you bought a $100,000 house for 5% down ($5,000) and the home appreciates 5% in the first year. After year one the home is now worth $105,000. Your home is worth $5,000 more and you only invested $5,000. That is a 100% return on your downpayment of $5,000, in just the first year. That is the power of investing in real estate. You get to keep all of the appreciation. Even though the bank gave you $95,000 to buy the home, they get none of that appreciation.

Opportunity Cost of Renting: No Loan Paydown

When you own a property with a mortgage, part of your monthly payment goes towards paying down the principal which reduces the amount of the loan. For a $450,000 property with a 6.625% interest rate, the principal reduction over 5 years can be calculated using an amortization formula, revealing a significant amount of equity built through loan paydown alone.

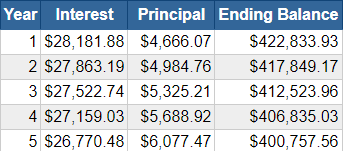

Take a look at the table below. This is pulled from an amortization schedule of the loan from the $450,000 house at 6.625% interest rate. You can find an amortization calculator easily on google. In the first five years you will pay the loan down $26,742 (the total of the rows in the “Principal” column). That number grows as the years go on and you pay more principal and less interest.

Now what about that interest number? You’d say “that’s a lot of money going to interest every year”. And you’d be correct, but your house hacking tenants will be paying for most of that. Furthermore, you can deduct the interest payments against your rental income. Something you can’t do with rent. We will factor in those large interest payments later in the blog.

Opportunities of renting: Put your down payment in another investment

With any investment you have to consider your opportunity costs. In other words, where else could you have put your money and would that have performed any better for you?

Alternatives to using your cash to buy a Home:

S&P 500 Index:

Assumption based on history: For the last 100 years this index fund has average annual returns of 10.13%. This sounds good, but as I will illustrate later in this blog, it pales in comparison to real estate.

Details: The stock market is known for its volatility. The high returns come with significant risk. For example, 1995 saw a 37.20% increase. But 2002 saw a 21.97% decrease. 2022 saw a 19.44% decrease. 2023 saw a 24% increase.

U.S. Treasury Bonds:

Assumptions: A very safe investment. It comes with its own assumptions, like any investment. The assumption here is that the US government will continue to be a government and will not default on its loans. Seems pretty safe compared to other investments.

Details: They are considered safer, but typically offer lower returns compared to stocks and real estate. Currently around 4-5% interest annually. And it doesn’t compound.

Overall numbers after 5 years of renting:

Assuming rent increases at 3.5% per year you will be paying $1,377/month in 5 years from now. Over the span of 5 years you will have paid $77,220 towards rent.

However, you’re $22,500 downpayment invested into the S&P index fund at our assumed rate of 10.13% compounded annually will be worth $36,236.48

Leaving you a net living cost of $36,236.48 – $77,200 = ($40,963.52)

Overall numbers after 5 years of house hacking:

Expenses include: Principal, Interest, Taxes, Insurance, Repairs/Maintenance, and Private Mortgage Insurance.

You will have paid $164,239.76 towards your principal and interest

You will have paid an estimated $20,914 in property taxes and insurance

You will have paid $5,400 in private mortgage insurance

You will have paid an estimated $10,859 towards repairs and maintenance

For a total expense of: $164,239.76 + $20,914 + $5,400 + $10,859 = $201,412.76

However, here are the positives to your net worth: Appreciation, Loan Paydown, Rent payments from Tenants

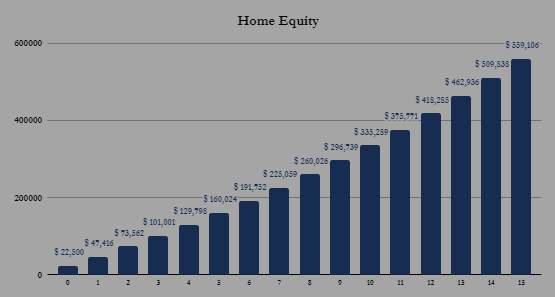

You’re home will have appreciated to an estimated value of 560,7812 an increase of $110,782

You will have paid down your loan by $26,742

Your tenants will have paid $154,439 in total rent

The total benefits add up to: $110,781.87 + $26,742 + $154,439 = $291,962.87

House Hacking net worth boosters minus expenses = $291,962.87 – $201,412.76 = $90,550.11

(The home equity for year five is calculated using the downpayment + appreciation + loan paydown)

House Hacking Vs Renting

House Hacking net worth after 5 years: $90,550.11

Renting net worth after 5 years: ($40,963.52)

Leaving you a net worth benefit of $90,550.11 – ($40,963.52) = $131,513.63

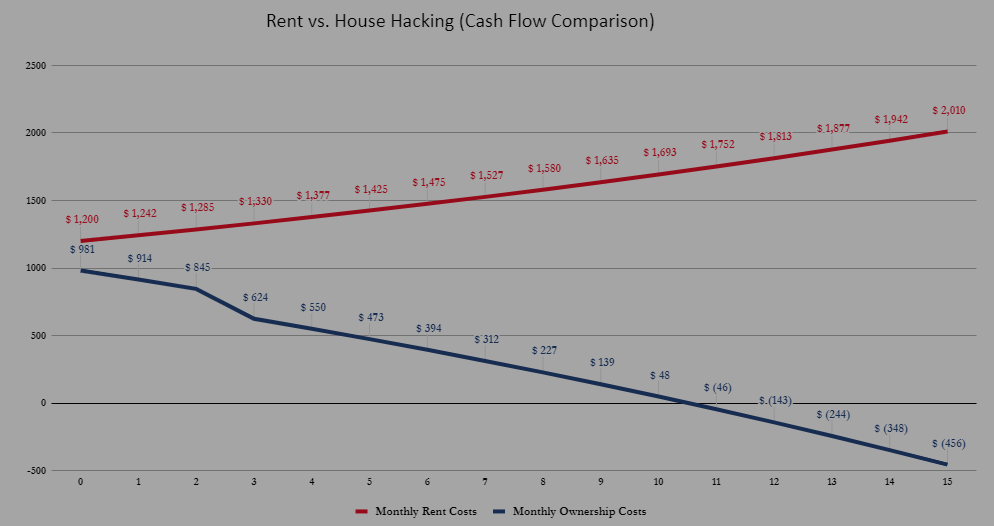

Here is a screenshot from our calculator on the difference in monthly payments between Renting vs House Hacking

The winner is clear. As rents continue to rise, renting will only cost you more money every year. House Hacking provides significant financial benefits through appreciation, loan paydown, rental income, and tax savings. The decision to rent or house hack should be informed by all of these factors, considering both the risks and the historical performance of the real estate and rental markets. We have an amazing rent vs house hack calculator that will do all of this math for you (pictured in graphics above). You can even change the assumptions for several factors (rent appreciation, home appreciation, rent payments, etc) if you think mine are too aggressive. Download the free calculator here.

After seeing these numbers our client’s often want to house hack, but are concerned they can’t afford the downpayment or qualify for a mortgage loan. They often do qualify and I bet you could too. Here is how!

- Concerned about downpayment. We work with downpayment assistance lenders that can give you a 0% interest loan to cover your downpayment. You only have to bring $1,000 to buy the home. If we negotiate seller credits you may even get paid to buy a home! You pay the down payment assistance loan back when you sell or refinance your home. It’s free money in the meantime. You can’t beat that!

- Concerned about credit? – You can qualify for a loan with a credit score above 500. Credit scores can actually be improved quite quickly. If you need to improve your credit score, we can introduce you to a credit repair program we work with.

- Concerned about qualifying? – set up a time to speak with us today about your debt and income and we can get a great idea in less than a day if you will qualify. It’s easy.

Extra thoughts:

- I did not include the cost to sell in this scenario because in this scenario we are imagining holding the property for longer than 5 years.

- Extra benefit towards house hacking:

Down Payment assistance – If you make less than 150k you can qualify for down payment assistance. This is a 0% interest loan for almost all of the downpayment required. You don’t have to pay it back until you sell or refinance your house. Let me say that again 0% interest loan.

3. This doesn’t include the potential tax benefits.

Total mortgage interest over 5 years = $137,497. This is deductible in proportion to the % of your home that is used as purely a rental (the bedrooms). Let’s assume the 4 bedrooms are 25% of the square footage of your home.

Let’s say you make $80,000/year and you are in the 22% tax bracket.

This will reduce the amount you have to pay on taxes over five years by: (Mortgage interest) x (tax bracket) x (the percentage of home used as rental) = $137,497 * 0.22 * 0.25 = $30,249.34 in tax savings.

https://www.irs.gov/publications/p936

https://www.irs.gov/help/ita/can-i-deduct-my-mortgage-related-expenses